This post may contain affiliate links, which means I'll receive a commission if you purchase through my links at no extra cost. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure policy for more information.

Pin for later. Follow on Pinterest.

INTRODUCTION

Paying off debt is one of the most challenging yet rewarding financial goals anyone can undertake. It requires discipline, patience, and a solid plan. As you pay off debt, you learn about money, habits, priorities, and what truly matters. Debt can feel overwhelming, but it doesn’t have to define your life. With the right mindset and strategies, it's possible to become debt-free and start building your dream financial future. My journey taught me many valuable lessons, and I hope sharing them will inspire and guide others on their path to crushing debt and reaching financial freedom.

MY “DEBT PAY-OFF” STORY

THE BEGINNING

My debt story began the night after graduation. I remember lying awake, anxious and overwhelmed, thinking about how I was going to handle thousands in debt with no clear plan. Thankfully, I had a job lined up and knew my income would increase over time, but my debt still worried me. But I didn’t want to wait for “someday” to fix my finances; I wanted to take action immediately. I decided to commit to a 7-year timeline to become “debt-free”. For me, 7 years felt achievable, and it allowed me the flexibility to change careers if I wanted, without debt holding me back.

FINDING HOPE AND A PLAN

After researching different debt payoff strategies, I discovered Dave Ramsey’s Total Money Makeover, which advocates the snowball method to pay off debt. Using the snowball method, I paid off the smallest debt balance while paying the minimum on the other balances. Then, when that first debt was paid, I applied that amount I paid to the next debt, and the next, and the next. Paying off that first debt balance changed my whole perspective on my debt, and I realized, “I can do this!”

I stuck to the snowball method, built up a 3-month emergency fund, and even created sinking funds for things I cared about, like travel and Christmas. In addition, I picked up ballroom dancing lessons to relieve the stress, which helped keep me balanced and motivated. I also calculated my net worth, which is a way to characterize your financial state as a “number.” The first time I calculated my net worth, my debt dragged it into negative territory, and I felt discouraged by how low the number was. However, as I paid each loan individually, I felt more confident that I could conquer my debt and watched my net worth grow.

THE TURNING POINT

Then, one of the most significant debt payoff milestones happened- the day your net worth was zero. The day my net worth hit zero—when I finally had more money than debt—was one of the happiest days of my financial life. I began by investing in my work’s retirement plan, gradually increasing my contribution while paying off debt and watching my net worth improve.

THE “AFTER DEBT” STORY

Finally, after years of hard work, I paid off my last debt and celebrated by opening a brokerage account to invest in my future even before my 7-year deadline. My net worth went from thousands in the negative to thousands in the positive! Fast forward, I stayed debt-free, planned a debt-free wedding after a 4-month engagement, and now share how to build wealth beyond the wedding through this blog.

My story might not be flashy, but it’s real, and I hope it will help others. Although I don't regret my debt payoff journey, there are things I would have done differently. Here are the lessons I learned from my experience with debt to inspire you on your journey.

LESSONS LEARNED FROM PAYING OFF DEBT

FACE THE REALITY OF YOUR DEBT

The first step was to come to terms with my debt. The total amount felt overwhelming, but knowing the exact number was necessary. When you calculate your net worth, you realize that all this debt is dragging down your financial situation. The bottom line is that it is hard to face the truth, but things will always stay the same once you do. By acknowledging the reality, I could finally make a plan to tackle it head-on. Facing my debt reality allowed me to map out a clear path to debt freedom.

TIP: You can’t fix what you don’t acknowledge. Knowing your debt number is the first step to conquering it. Also, calculate your net worth. Several budgeting apps like Simplifi will calculate your net worth, track your spending, achieve your saving goals, and pay off debt.

CREATE A VISION FOR YOUR DEBT-FREE LIFE

I needed a clear vision or “big why” for paying off debt. For me, my big why was feeling freedom. Freedom would allow me to travel more, have more autonomy in my career, date, marry, travel, build wealth, and enjoy life. Maybe your big “why” is setting an excellent example for your kids, being able to leave an inheritance, or just feeling freedom, too. Without a solid reason to pay off your debt, it just won’t happen.

TIP: Visualizing your debt-free future can motivate you, even on tough days. Define your “big why” for paying off debt by thinking, “I could do _____ if I had no debt” or “I could feel ______ without my debt.” It helps to remind yourself why you’re making sacrifices today.

SET A REALISTIC TIMELINE FOR YOUR LIFE CIRCUMSTANCES

I committed to a 7-year timeline because I knew I would have times I could hustle to pay off debt and times when I just needed to survive the day. This goal gave me something to work toward, and having a timeframe made my journey more structured. It also motivated me to stay focused because I could see an endpoint. I wish I could have paid off $100,000 in 10 months, but that was unrealistic for me at the time.

Life happens, and you must respect where you are and work with what you can handle physically, mentally, emotionally, spiritually, and financially. Don’t beat yourself up if you can’t pay off $30,000 of credit card debt in 6 months because you are working on your college degree while trying to raise 3 children under the age of 5. Have a goal, but have a goal that works for your life.

TIP: Set a realistic debt-free goal based on your current and future circumstances. Giving yourself a timeframe to stick to without feeling burned out is essential.

MAKE YOUR BUDGET WORK FOR YOU

I tried different budgeting methods—like the envelope system, zero-based budgeting, using budget apps like YNAB, and the reverse budget—until I found what worked best for me. Having a budget that fits my lifestyle made it easier to stick to my plan.

One thing that people don’t talk about is how your budget changes as your life changes. Starting with the 50/20/30 budget or a zero-based budget is excellent; however, as I learned my spending habits, I realized these types of budgets just frustrated me at the end of the month. No month of spending is the same. However, if you can plan out your fixed and day-to-day expenses and plan for irregular or surprise expenses, you can create a budget that works for you.

The biggest thing that helps when starting a budget is tracking your spending for 1-3 months. Budgeting apps or your bank statements are great for this; now, I use an Excel spreadsheet and Simplifi. Once you know your spending patterns, you can create a budget based on your spending categories and debt payoff plan.

TIP: Track your spending and find a budgeting style that fits your personality and lifestyle. There’s no one-size-fits-all solution, so don’t be afraid to try different methods until you create the perfect money system.

CONSISTENCY WITH A DEBT PAYOFF STRATEGY IS KEY

I followed Dave Ramsey's “Total Money Makeover“ and used the snowball method for my school loans. I started with the smallest debt and worked my way up, gaining momentum with each win. Dave Ramsey also recommends paying off the principal balance on the debt because the interest relies on the principle. If your principle is lower, then the interest growth will slow down. This tip and the snowball method helped me pay off debt even faster.

Seeing debts disappear, one by one, was incredibly encouraging. I realized that consistency with a strategy and seeing results are more important than the actual strategy. Picking a debt payoff strategy that works with you and that you can stick to, especially when things are hard, is how you pay off debt.

Now that I’ve learned more about personal finance, I discovered several methods to pay off debt, like the avalanche method, which focuses on paying off the highest interest rate first. If I had credit card debt with a 25% interest rate, that would have kept me up more at night, and I probably would have chosen the avalanche method to get rid of debt.

TIP: Choose a debt payoff system that works for you and stay consistent. Whether it’s the snowball method or another strategy, consistency is critical. Each small victory boosts your confidence and keeps you going.

BUILD AN EMERGENCY FUND

Dave Ramsey’s system advocates setting aside an emergency fund even while paying off debt. Creating an emergency fund helped me avoid relying on credit cards when unexpected expenses arose. It gave me peace of mind knowing I had a safety net and didn't have to rely on a credit card or loan if I needed to buy a new car after an accident.

In addition, it helps to have an emergency fund at a separate bank so that you are less tempted to spend the money. It also helps to put your emergency fund in a high-yield savings account so that the interest in the account grows and works in your favor. I’ve used Sallie Mae for an emergency fund, and Ally Bank is also popular.

Starting with an emergency account of $1000 can help prevent you from using credit cards if you need new tires. Then, you can save just 1-10% of your income for your emergency fund every month, and the account will grow until you reach your goal.

TIP: Have a safety net to protect yourself from financial setbacks while paying off debt. A small emergency fund starting at $1000 can prevent you from slipping back into debt when life throws you a curveball. It may feel challenging to save for an emergency fund while paying off debt, but you will rely on debt if you don’t have some financial cushion for things that happen in life.

While paying off the minimums for all your debt, focus on getting a primary emergency fund as fast as possible. If you need help building an emergency fund, try cutting expenses like subscriptions, a no-spend month, or other saving challenges to boost your emergency fund. Once you reach at least $1000, you can set a portion of your income to savings and then focus on crushing your debt.

USE SINKING FUNDS TO SAVE FOR THINGS YOU WANT IN LIFE

Sinking funds, or “intentional saving accounts,” to save for specific expenses like car repairs, Christmas gifts, or a wedding. This way, you never have to dip into your regular budget or use credit. Sinking funds also help you plan for unexpected expenses that creep up, like your annual insurance premium, which always comes up at the time of year when you feel the most stressed about your money. Instead, you transfer funds from your sinking fund to cover the expense and move on with your debt pay-off plan.

Just like the emergency fund, keep your sinking funds in a separate account in a high-yield savings account. For our wedding, my partner and I created a joint account at Wealthfront dedicated to our wedding, which had over 4% interest at the time, so our money was growing even faster.

TIP: Plan for predictable and planned expenses by saving small amounts regularly. Use a high-interest savings account for sinking funds like Christmas shopping, car repairs, or weddings.

AVOID TAKING ON MORE DEBT

I decided to avoid credit cards entirely during my debt payoff journey. Honestly, I didn’t even use a credit card until I paid my debt. I didn’t want to undo my hard work by adding new debt to my list. That meant sticking to cash, debit, or prepaid cards for all my expenses. Using the envelope system early on and sinking funds for irregular expenses helped me avoid debt. Envelope budget wallets like this one are great for keeping your cash organized and avoiding using credit cards.

TIP: Break the cycle by taking action to avoid debt, even if it means making sacrifices. Avoiding new debt is essential to making progress on your payoff plan.

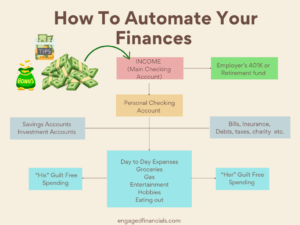

AUTOMATION IS KEY TO PAY OFF DEBT WITH EASE

One of the best strategies I adopted on my debt-free journey was automating my payments. By setting up automatic transfers, I ensured that a portion of my income went directly to my monthly debt payments without thinking about it. Automation reduced the temptation to spend that money elsewhere and kept me on track. Automation simplifies the process, reduces stress, and ensures consistency, making it easier to stick to your debt repayment plan and reach your financial goals.

TIP: Automate your finances as much as possible. If you don’t know how to call your bank or the company, ask how to do “bill pay” or automatic payments. Sometimes, your bank can “automate” payments by sending checks to a company to help you make sure you make the payments.

GET CREATIVE WITH SAVING AND HAVE FUN MANAGING MONEY

I enjoy spending money but love finding ways to save money to pay it later. It may be a mental game that I use to get myself to save, but it works. Looking for ways to save money also helped me pay off debt faster with the savings. Cutting things out in your budget, like subscriptions you don't use, can help you save money. Apps like Rocket Money can help you cut subscriptions and manage your finances all in one place.

You can find fun ways to save, like using coupons, finding discounts, thrifting, and cashback apps like Rakuten online or Ibotta for grocery savings. The Capital One Shopping app also has a great app that helps you save money and use coupons for free. Or, try savings challenges with all the Pinterest or Etsy calendars to make saving more money fun. Check out these saving challenge binders on Amazon.

TIP: Find small ways to save every day. It all adds up and can make a big difference over time.

GET SMART ABOUT YOUR TAXES

If you get a tax refund every year, using your refund towards your debt is a great way to pay off debt faster. I treated it as a “bonus” opportunity to make a more significant dent in my balance. I also looked for tax deductions to maximize my returns, such as giving to charity or investing in your 401K.

TIP: Plan for tax season and use refunds strategically. They can be a great way to accelerate debt payoff or boost your savings.

GIVING ENHANCES ABUNDANCE

Being generous helped me feel more abundant and kept me grounded. It reminded me that there’s more to life than money; generosity brings joy, and you can help organizations that are meaningful to you. Giving to charities also helps in other ways, like giving you tax breaks to help you save money.

TIP: Giving can be part of your financial plan, even when paying off debt. It helps create a positive mindset around money, lowers taxes, and reminds you of the bigger picture.

TREAT CREDIT CARDS LIKE DEBIT CARDS

After I paid off my debt, I got a cashback credit card and paid it off every week. I used it like a debit card, never carrying a balance. It allowed me to earn rewards without the risk of accumulating debt. However, if you have a lot of debt or can’t pay off your card monthly, avoid credit cards.

TIP: Credit can be a tool if used wisely, but only after you’ve built good financial habits. Treat it like cash, and don’t let the balance carry over.

LEARN ABOUT MONEY

Growing my knowledge helped me build wealth faster and make informed decisions. I would listen to audiobooks on Audible while driving to work and read so many books to help me learn more about money. Even while paying off debt, you can always discover ways to make money work for you.

I learned more about investing and the stock market by reading “A Random Walk Down Wall Street” by Burton Malkiel, which was an entertaining way to understand how markets work, discover investing options like index funds or target date funds, and learn how to build wealth with consistent investing rather than trying to time the market. If you need more inspiration, check out the Engaged Financials Suggested Reading Page for inspiration on mindset, budgeting, money systems, and investing.

TIP: The more you know about money, the better you can manage and grow it. Educate, empower, and encourage yourself on your debt-free journey by reading books. There are always new strategies and tools to explore. Try audiobooks or podcasts to learn more about money to help you grow wealth while crushing your debt. You can even go to the library and rent audiobooks for free in some instances.

INVESTING 1% OF INCOME WHILE PAYING OFF DEBT IS A GOOD IDEA

Even when I focused on debt, I started investing some of my income in an IRA, but I didn’t invest in my employer's retirement plan because I wanted to focus on being debt-free. However, I wish I had invested just 1% of my income toward my employer's retirement plan while paying off debt. I wouldn’t have missed that 1% of my income, and compound interest would have grown much sooner.

Another popular money system that advocates investing up to your employer's match for the 401k before paying off even high-interest debt is the Financial Orders of Operation (FOO) by The Money Guys and the book “Millionaire Mission“. Why? Because the employer will match your 3-5% of income, you can still pay off your debt and likely won't miss the money. It is “free money” towards your retirement while paying off debt and starting small, which makes it manageable.

Are you still nervous about investing? One way to ease into investing regularly is using Acorns, which rounds up your change and helps you invest it. Over time, you can see how your change can become thousands of dollars. I tried it, and over the last couple of years, my change has grown beyond what I had imagined. It is fun to watch my change grow simply because I'm investing with Acorns.

TIP: Start small, but invest in your employer's retirement as soon as possible, especially if a match program exists. Even 1% makes a difference over time. Waiting can cost you more in the long run. You can invest in an IRA and look at self-employed retirement plans if you are self-employed. Places like Fidelity allow you to invest for as low as $25-50 per month.

When you invest, make sure the money goes into the investment account and does not stay in the default cash account (otherwise, it won't grow much). If you want to invest more easily or feel scared, try Acorns to watch your change work for you and grow. However, I am not a financial advisor, so please do your research, learn about investing, and understand the risks.

If you are wondering whether to pay off debt or invest, research what makes sense for you and do what will help you sleep better at night. If investing 1% while paying off debt enables you to sleep better, do it. On the other hand, if paying off your debt with everything helps you sleep better, do it. This is your journey; do what is best for you.

TRACK YOUR PROGRESS WITH YOUR NET WORTH

I tracked my net worth and celebrated the day it hit zero because I knew it would only go up from that point. I still tracked my net worth while paying for my wedding, which grew because I avoided debt. The first time you look at your net worth when you start your debt payoff journey, it can be very sad and discouraging. But it is just a number, and the faster you pay down debt, the faster that number will grow.

TIP: Monitor your progress to stay motivated by tracking your net worth. It’s gratifying to see how far you’ve come, and it keeps you engaged in your journey.

FOCUS ON EARNING MORE MONEY

One way to pay off debt faster is to make more money at your primary job. Figuring out what you need to do for a raise can shape your career path so that you earn more money from advancing your career. If you haven’t negotiated for a raise, start working on this while paying off debt to increase your income. This extra money allowed me to pay off debt faster and invest more.

It’s a common misconception that making more money will solve all your financial problems, but it often leads to more expenses without addressing overspending habits. I realized that even as my income increased, my spending could quickly match it if I wasn't careful. True financial freedom comes from controlling your spending, not just boosting your earnings. It's essential to set boundaries, stick to a budget, and understand what triggers your spending to avoid falling into the same traps.

TIP: Work to earn raises in your career. It can accelerate your financial goals and open new doors for financial freedom. However, remember that making more money won’t cure your overspending.

SURROUND YOURSELF WITH LIKE-MINDED PEOPLE

I spent time with people who were also working on their finances. Their support and encouragement were invaluable. Sharing tips and experiences helped me stay motivated and inspired. Find “money mentors” who can guide you on crushing your debt, managing money, and growing your wealth. You don’t have to be best friends with Warren Buffett. Read books, listen to podcasts, read blogs, go to conferences, make friends, and find money mentors.

TIP: Choose friends who will uplift you and help you towards your financial goals. Positive influences make the journey easier.

TAKE TIME TO CULTIVATE JOY IN YOUR LIFE

Even while paying off debt, I found affordable ways to enjoy life. Whether taking a weekend road trip or taking a dance class, I found ways to have fun. Paying off debt is important, but if that is the only thing you have to look forward to, you may start overspending to make yourself feel better after a while.

TIP: Being on a budget doesn’t mean your life has to be boring. Find creative, low-cost ways to bring joy to your life, even when focused on financial goals.

YOUR MINDSET MATTERS

Throughout my journey, I realized that a positive, growth-oriented mindset was more valuable than any amount of money. Believing I could reach my goals was half the battle. Otherwise, you feel overwhelmed by the debt cycle where your debt feels like it's growing, and you feel helpless to stop it. Your thoughts about money matter because they influence your actions, which leads to better results. Even when earning more money, I felt more stressed about my finances because my thoughts were focused on overwhelm and scarcity. It wasn’t until I shifted my mindset and started taking consistent action that I saw progress and avoided the debt cycle.

By changing how I thought about money and debt, I could see evidence of improvement, which built my confidence and eased my worries. Ultimately, it’s not just about how much you earn but how you approach your finances that makes the biggest difference.

TIP: Your mindset determines your financial success. Cultivate a positive attitude, and don’t be afraid to invest in yourself.

CELEBRATE MONEY WINS

Every time I paid off a debt, I celebrated. It might have been a small celebration, but it helped me stay motivated. Whether it was a special treat or a simple night out, these rewards kept me going. Even if it is celebrating with your money friends and mentors, your little victories matter. If you don't take time to celebrate your wins, you will feel miserable on this debt payoff journey.

TIP: Reward yourself for small milestones to keep the momentum going. Recognizing your achievements makes the process feel manageable.

ENJOY BEING DEBT-FREE AND CHOOSE TO LIVE A DEBT-FREE LIFESTYLE

Once I finally paid off thousands of dollars before my 7-year goal, I committed to staying debt-free. My money is building my future, not paying off the past debts. Having the freedom to enjoy life and not worry about debt is priceless.

TIP: Debt freedom is a lifestyle choice. Once you’re out, don’t fall back into old habits. Protect your hard-earned progress and continue building wealth.

CONCLUSION

Paying off thousands of dollars in debt wasn’t easy, but it was worth it. Along the way, I learned that you must be intentional, disciplined, and willing to change your mindset. Being debt-free has given me peace of mind and the freedom to invest in my future, have a wedding debt-free, and enjoy life without stressing about money. Cheers to being debt-free!

What lesson inspires you the most for your debt payoff journey?

Pin for later. Follow on Pinterest.