This post may contain affiliate links, which means I'll receive a commission if you purchase through my links at no extra cost. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure policy for more information.

Pin for later. Follow on Pinterest.

INTRODUCTION

Are you worried about paying off debt? In America, the U.S. household debt grew by $733 billion dollars in 2024, and this enormous amount of debt is straining relationships. Whether you just graduated college with school loans or paying for a wedding, debt can be a significant burden on your finances. However, if you don’t pay off debt, you can get trapped in the debt cycle, where you keep using debt to pay for your lifestyle and can’t afford it.

While debt can be a huge stressor for couples, tackling it as a couple can bring you closer and set you up for a secure future. If you and your partner are facing any debt, here are 10 helpful steps to get you both on the same page to discuss debt openly and work toward financial freedom together.

HOW TO TALK ABOUT DEBT WITH YOUR PARTNER AND PAY IT OFF TOGETHER

1. SET GROUND RULES FOR DEBT DISCUSSIONS

When you start talking to your partner about money, you want a productive discussion without getting into a fight. The debt is a fact, and now you want to work together to become debt-free. You can break free from the debt cycle together as a couple by just starting to talk about debt.

Set some ground rules about how you will talk about money and debt. Talking about debt with another person can feel very vulnerable, so agree to approach debt discussions with respect, openness, and patience. Do not shame or blame your partner or yourself for the debt. Avoid interruptions or judgments, making sure each person feels heard and valued. Ask questions like, “How can we set ourselves up for a better future?”

Lastly, set a goal and a time for the conversation. If you have an objective like “I want to talk about how much debt we both have and what we are doing about it,” it is more helpful than “We need to talk about our debt.” Next, establish a time for both you and your partner to discuss your debt and how long the discussion will take. From my personal experience, I recommend no longer than 1 hour for these money discussions because the more tired you get, the more likely you will become disengaged from the conversation or want to fight.

2. IDENTIFY MONEY GOALS AS A COUPLE

Identify a shared purpose for becoming debt-free and why you want to pay off debt. When I paid off my debt, having the goal drove me to stick with the plan. A vision for your life as a debt-free couple can encourage you to be consistent with your debt-free goals. Maybe you want to be debt-free as a New Year goal. Or, your vision could be saving for a home, having a debt-free wedding, or retiring early to travel the world. A common goal motivates you both, especially when things get tough.

During this debt-free vision session, have an open conversation about your relationships with money. Asking open-ended questions about your experiences with debt can reduce misunderstandings and build empathy. Ramit Sethi, author of I Will Teach You To Be Rich, discusses these topics on his Money for Couples podcast to help couples open up about money to each other. Why? Because your thoughts, feelings, and experiences with money influence your actions more than the amount of money you have. For example, ask your partner, “What does money mean to you? Do you have any fear or anxiety around money?” Questions like these can help you understand each other’s backgrounds, experiences, and values regarding money.

3. PRACTICE GOOD COMMUNICATION TECHNIQUES WHEN TALKING ABOUT DEBT

Try to start talking about your money as a tool to serve you both as a couple. Instead of using phrases like “my money” or “your debt,” try using words like “our money” or “our debt” to foster a sense of teamwork and a shared understanding. This small language change can significantly affect how you approach each other and your debt. Avoid statements that could feel accusatory when discussing debt, like “You never…”, “You always…” or “Why did you…” Instead, use “I” statements, such as, “I feel stressed when we have high-interest debt,” which allows you to express your feelings without blaming your partner. This approach helps create an open, shame-free environment for talking about debt.

Money is just a tool, but talking about money will likely reflect your baseline communication pattern. If you need help having productive and crucial conversations, try reading the book Crucial Conversations by Kerry Patterson et al. It gives tips on how anyone can have productive discussions, no matter the topic.

If the debt discussion gets heated or you feel shamed or angry, stop the discussion and schedule it for another time. Consider having a “safe word”, a random agreed-upon word that, when said, things stop. A “safe word” is a quick way to take a break before discussions overwhelm you. For example, you feel angry about your partner criticizing you about how you spent money last night. But instead of yelling back about how he spent money on a 4-wheeler with the credit card last month, you use your safe word, “peanuts.” You both stop and agree to discuss things later when you are calmer.

If you can’t talk about debt without getting into an argument, that is a time to bring in help. Get a finance coach, counselor, or certified financial planner to help you work through your money discussion and finally pay off debt.

4. LIST ALL DEBTS AND PRIORITIZE THEM

Make a comprehensive list of all debts, including balances and interest rates. Include credit cards, student loans, auto loans, and personal loans—with their outstanding balances, interest rates, and minimum payments. Knowing these details helps you decide which debt to prioritize first.

Next, calculate your net worth by listing all assets (cash, savings, investments, real estate, and valuable personal items) and subtracting your total liabilities (all debts). Tracking your net worth regularly allows you to measure progress, see the financial impact of debt repayment, and set meaningful goals for building wealth. Even if this is a huge negative number, you can improve your net worth by paying off the debt and stopping accruing more debt.

5. CHOOSE A DEBT PAYOFF STRATEGY TOGETHER

Decide on a debt repayment strategy to pay off debt that works for you as a couple and addresses your debt priorities. There are several approaches and opinions about debt and debt payoff. Should you pay off student loans? Should you invest first? Do you need to pay off high-interest debt first or start with the lowest balance to motivate you? The most important question is, “What is your biggest worry about debt, and which plan can help you address it?”

Perhaps you have a lot of school loans but feel overwhelmed and don’t know where to start. The snowball method may help relieve your feelings of being overwhelmed, as it focuses on paying off the lowest debt balance so you can get momentum to pay off debt. Dave Ramsey’s “Total Money Makeover” recommends the snowball method to pay off debt to help people stay motivated, which I used to pay off thousands in debt.

However, if you have a lot of credit card debt with interest rates over 8%, paying that off as soon as possible may help you sleep better at night so that the interest isn’t making you pay more than the original balance. With high-interest debt like credit cards, the avalanche method focuses on high-interest debts for maximum savings and may help you crush credit card debt.

6. TRACK YOUR EXPENSES AND CREATE A BUDGET

Tracking your expenses is a critical step toward paying off debt because it gives you a clear picture of where your money is going. By categorizing your spending, you can identify unnecessary costs and areas where you might overspend. With this knowledge, you can create a budget prioritizing debt repayment while covering your essential expenses. Making a budget as a couple will help you allocate funds intentionally so you can direct more money toward paying down debt. The biggest key is to find a budget, learn as you make a budget together, and create a money system that works for you.

Consider using a budgeting app like Simplifi to manage your finances together. Simplifi lets you create a spending tracker, monitor savings, and show your net worth on each account. For financial accountability, you can “share” each other’s accounts. Monarch Money can combine your net worth and show individual spending. With shared access, you can stay updated on spending, saving, and debt progress, promoting accountability and teamwork.

Set up a joint budget that prioritizes debt repayment and essential expenses and includes a little “fun money” to keep things enjoyable. A shared budget becomes your roadmap, helping both of you stay on track without feeling deprived. For joint expenses, consider contributing based on income percentages rather than 50/50 if your incomes differ vastly. If you make more than your partner and wonder how to manage your money together, read the book “When She Makes More” by Farnooshi Torabi. She illustrates female breadwinners' struggles and shares stories and tips on managing money successfully as a couple.

7. START AN EMERGENCY FUND AND SINKING FUNDS TO AVOID MORE DEBT

Many people can't come up with $1000 for an emergency and will use credit cards to cover the costs. The more unexpected things that happen that you haven’t saved for, the more likely you are to use debt. To avoid debt, create an emergency fund and sink funds. Starting an emergency fund, even if it's just $1,000, can provide a safety net for unexpected expenses, preventing you from adding new debt. Aim to build this up to cover a few months’ expenses as you pay off debt.

After creating an emergency fund, create separate sinking funds for predictable but irregular expenses like car repairs, Christmas gifts, or savings for a wedding or a honeymoon. These small savings pools prevent you from reaching for credit cards when these expenses arise.

Another tip is to create emergency and savings funds and put them in a separate bank from the one you use for day-to-day spending. That way, you have to log into the account, and it gives a “check” from reflectively using the money. My husband and I set up a high-yield savings account at Wealthfront for our wedding as a family emergency fund. With high-yield savings accounts, the interest adds up faster than a traditional bank account, so it is growing in the account every month. Banks like Sallie Mae, Ally Bank, and Capital One have great high-yield saving account options. Just make sure you check the interest rate on the account and that the account has FDIC insurance.

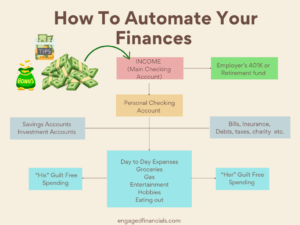

8. AUTOMATE YOUR FINANCES

Automating your finances helps simplify your finances and debt strategy process and ensures consistency. Automating your money elevates your budget into a money system that works for you. By setting up automatic payments for your bills and debts, you eliminate the risk of late fees and missed payments.

To automate your finances, start by linking your bank account to your creditors and scheduling recurring payments for your monthly bills and debts, such as credit cards or loans. You can also automate savings by directing a portion of your income into a separate account dedicated to debt repayment, allowing you to build up funds without the temptation to spend them. This structured approach helps you stay on track and fosters a sense of control over your financial journey.

9. REGULARLY MEET TO TALK ABOUT MONEY

Schedule regular “money dates” to review your finances, celebrate wins, and check in on your debt progress. You will not resolve your debt in one conversation, so be patient and have these money talks about debt over several money dates. Have time every week to discuss your debt, finances, money goals, or any other money topics during your date. If you haven’t discussed your debt in a long time, you may need an hour for a financial check-in. You can have fun with your money dates by going to coffee shops or visiting hotel lobbies to stay inspired. Keeping these discussions relaxed and positive helps make them something you both look forward to rather than a source of stress.

10. CELEBRATE SMALL WINS ALONG THE WAY

Paying off debt can be a long journey, so celebrate each small win. Tackle debt in small steps, like paying off one specific balance or reducing a particular expense. Watch your net worth grow as you pay off debt. By breaking down large debts into smaller, achievable milestones, you can celebrate each “mini-win,” reinforcing positive teamwork. A team-focused approach avoids placing blame and strengthens your relationship. Plus, acknowledging these milestones keeps you motivated and reinforces positive financial habits.

CONCLUSION

Paying off debt as a couple is a journey that requires commitment, understanding, and teamwork. By setting shared goals, creating a practical plan, and celebrating your progress, you’ll reduce debt and build a stronger relationship and financial future. Each step brings you closer to the life you both hope for—debt-free and ready to achieve your dreams together.

IN SUMMARY

How to Talk About Debt With Your Partner and Pay It Off Together

- Set ground rules for debt discussions.

- Identify money goals together as a couple.

- Practice good communication techniques when talking about debt.

- List all debts and prioritize them.

- Choose a debt payoff strategy.

- Track your expenses and create a budget. Consider budget apps like Simplifi and Monarch Money to help pay off debt and achieve money goals.

- Start an emergency fund and sink funds to avoid debt. Get a high-yield savings account with an online bank with FDIC insurance, such as Wealthfront, Sallie Mae, Ally Bank, and Capital One.

- Automate your finances.

- Have money dates with your partner.

- Celebrate small wins along the way.

Are you ready to talk about debt with your partner?

Pin for later. Follow on Pinterest.