This post may contain affiliate links, meaning I’ll receive a commission if you purchase through my links, at no extra cost. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure policy for more information.

Pin for later. Follow on Pinterest.

INTRODUCTION

Life can be hectic, and your finances will be chaotic if you don’t manage your money intentionally. A budget helps bring order to your finances; without it, there’s a higher risk of spending beyond your means, ending up in debt, or neglecting future goals. For example, if you are planning a wedding or any major life event, it’s easy to focus solely on the big day. However, a personal budget is essential for keeping your long-term finances intact. While a “budget” may seem daunting or constricting, you can create a system that makes your money work for you. In this blog post, I’d like to share how to make a budget and create a budgeting style that helps you manage your money.

BASIC ELEMENTS OF A BUDGET

A budget is a method to show you how much money is coming in, where it’s going, and what’s left. There are basic elements of a budget; once you know these elements, you can create a budget that works for you. The essential elements of a budget are the following:

- Income: This is all the money that you make in a month. Whether you have irregular income, passive income, side hustle income, or regular income from a job, you need to know your income or “budget input” because your income needs to cover your expenses.

- Fixed (or Regular/Routine) Expenses: Non-negotiable bills like rent/mortgage, utilities, insurance, etc. If your income can’t cover your expenses, then your budget shows you where you may need to cut from your expenses.

- Day-to-Day (or Discretionary) Expenses: Flexible costs, such as groceries, dining out, entertainment, and transportation.

- Savings and Investments: Money used in emergency, retirement, and investing funds.

- Debt Payments: Regular payments for student loans, credit cards, or personal loans. Once you (and your partner) pay off debt, you can move money to other elements like saving and investing.

- Irregular or Periodic Expenses: These are costs that don’t happen every month but come up in the year, like car maintenance, Christmas, a honeymoon, or annual insurance payments.

- Financial Goals: Your budget needs to support your short-term and long-term goals, such as saving for a wedding, making a down payment on a home, or saving for a vacation.

- Tracking Method: Use a tool or system to monitor spending.

Each of these elements helps create a complete picture of your money's spending. Once you have the essential elements, you can start making a budget.

HOW TO MAKE A BUDGET

Your budget tells the story of how you use money, where it is going, what it is doing, and how it works for you. Here are the simple steps for making a budget that works for you.

1. Set Your Goals

Decide what you want your budget to accomplish beyond just paying bills. Define short-term goals (like saving more money for a wedding) and long-term goals (like retirement or buying a house). These will guide your budget and help organize your money to accomplish these goals.

2. Calculate Your Income

Know your monthly take-home pay and any other income streams. This number is the foundation of your budget. Even if you have irregular income, you can take the average of your income from the last 3 months to get an “income” number.

3. Organize Your Expense

Organizing your expenses is crucial in creating a budget that works for you. By categorizing your spending into groups, you gain a clearer picture of where your money is going each month. This organization helps you identify areas where you may need to spend more wisely and allows you to prioritize your financial goals. For example, once you separate your essentials from discretionary spending, you can easily see where to cut back or allocate more toward savings. Here are the spending groups to consider:

- Fixed (or Regular/Routine) Expenses: These include housing, bills, insurance, debt, and loan payments.

- Day-to-Day (or Discretionary) Expenses: Covers groceries, gas, hobbies, date night, eating out, and entertainment.

- Irregular Expenses: Set aside money for house repairs, holiday gifts, annual insurance premiums, or subscriptions.

- Saving and Investing: Treating saving and investing as “expenses” ensures that you prioritize automatically allocating a portion of your income to building wealth before spending on other discretionary items.

4. Choose A Tracking Method For Spending And Saving

Tracking your spending can illustrate what your money is doing. Budgeting apps like YNAB and Simplifi can help you easily track your spending, provide insights, and report on how to reach your financial goals.

5. Make Adjustments As Necessary

Creating a routine to reassess your budget is critical to ensuring it stays aligned with your life and financial goals. You adjust your budget accordingly as circumstances change—whether due to a new job, unexpected wedding expenses, or shifts in your priorities. Set aside time each week or month to review your income, expenses, and goals, and make adjustments where necessary.

FIND YOUR BUDGETING STYLE

Creating a sustainable budget starts with understanding your “budgeting style.” Just as there are different learning styles, some budgeting methods work better for certain personalities and needs. Finding your budgeting style helps you create a natural system, whether you like tracking every cent or a general approach. It will take time, but you will find a budget style that suits your needs. You can even merge elements of one style to create a money system that works for you. Here are popular budget systems to consider:

Traditional Budgets

Track each dollar spent through detailed spreadsheets or notebooks. This method clarifies exact spending and is effective for those who want to monitor all categories closely. For example, I created a simple Excel spreadsheet to track my spending as a part of my budget style. It captures categories that are important to me and keeps me organized. In the book “Get Good with Money” by Tiffany Aliche, she explains how budgeting can be helpful and fun. She also has excellent spreadsheets to help you create a simple and effective budget.

Zero-Based Budgeting

The zero-based budgeting approach, popular with tools like YNAB, allocates every dollar in your budget, ensuring that all money has a clear purpose. It’s helpful if you want a structured and intentional plan for every dollar. When I first started budgeting, I used the zero-based budgeting method to help me track and correct overspending. Zero-based budgeting also helps you develop intentional spending habits to pay off debt, build savings, and consistently invest for your future.

Cash Envelope System

In the cash envelope or “cash stuffing” system, you physically put cash into envelopes for each spending category (like groceries or entertainment). The “cash stuffing” system works well to keep spending in check and is good for curbing overspending because, once the envelope is empty, you can't spend more money on that category. The envelope system is also used in Dave Ramsey's money program and his book, “Total Money Makeover.” He also has a budgeting app called Every Dollar so that every dollar has a purpose in your finances. Try using cash envelopes as a budgeting style with products like these.

Percentage-Based Budgeting

Percentage-based budgeting or spending plan is excellent if you prefer a more flexible approach that doesn’t track every expense closely down to the dollar. Assign portions of your income to categories like needs, wants, and savings. For example, the typical “50/30/20” rule divides your income, where 50% goes to needs/essentials/fixed expenses, 30% to wants, and 20% to savings. Another example is “60/30/10,” which splits your income into 60% for needs, 30% for wants, and 10% for savings. Use percents that work for you. For example, if you live in a high-cost-of-living area where your house is 35% of your income, the 60/30/10 rule may work better than the 50/30/20 rule.

Ramit Sethi applies percentage-based spending in his Conscious Spending Plan in his book “I Will Teach You To Be Rich.” The Conscious Spending Plan helps simplify your finances into fixed costs, savings, investing, and “guilt-free “spending and uses percentages for each category. If one category is high, then you must adjust your spending. For example, if your fixed costs are at 90%, you'll likely feel stressed about money and need to cut some of your budget.

Reverse Budgeting

The reverse budget is a system in which you prioritize saving first, also known as “pay yourself first,” and then the rest takes care of your spending. It’s perfect if you’re focused on saving and investing goals. I used the reverse budget to help build wealth while planning my wedding. On my Excel spreadsheet, saving, charities, and investing are at the top of the spreadsheet, so these categories are the first that are funded in my budget. The rest of the money is what I live off of.

The “Plan Ahead” System

Popularized by Fiscal Fitness Phoenix, the “Plan Ahead” system emphasizes creating a budget that covers future expenses and goals. This approach focuses instead on consistently saving for fixed, day-to-day, and irregular costs.

Account Buckets System

The account “bucket” system is great for those with irregular income, those who have tried several different budgets, or those who don't want to track every dollar. This method uses separate accounts for specific goals and needs, such as bills, savings, and discretionary spending. The goal is to use money to fund these accounts, which pay for your bills, debts, savings, investing, and day-to-day expenses without you having to think about it.

The Profit First system by Mike Michalowicz is a way to manage business finances using a similar “bucket” system. However, this book also applies to personal finances because it prioritizes “paying yourself first” and allows you to see where your money is going. It also allows you to manage money effectively with account buckets to stay organized without going crazy.

PLAN FOR FUTURE PURCHASES

Budgeting isn’t only about managing current spending. It’s also about preparing for future expenses with dedicated savings. Consider the following accounts in your budget:

Emergency Fund

Start saving 1-10% of your income into a separate monthly emergency savings account. You want a bank different from your regular bank to decrease the temptation to spend this money. Gradually, you will earn $1000 for emergencies and reduce your reliance on credit cards if something happens. Ultimately, setting aside at least 3–6 months’ expenses for unexpected events is essential. This buffer can prevent you from going into debt during unforeseen challenges like medical bills or job loss.

Sinking Funds

Separate funds for predictable but irregular costs (like car maintenance or holiday gifts), or sinking funds, ensure these expenses don’t derail your budget. You can set up sinking funds as small monthly contributions that grow over time.

Upcoming Goals

Include your upcoming goals in your budget. Save for anticipated costs, such as a wedding or down payment, and keep in a separate account from your emergency fund or day-to-day spending account. Don't forget about investing regularly. This will allow your money to grow over time.

MAKE MONEY WORK FOR YOU

A budget isn’t just about paying bills—it’s about using money intentionally to create the future you hope for. The big key to an effective budget is making money work for you within your money system. Here are some ideas to help make your money work hard for you:

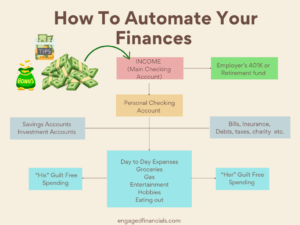

Automate Payments and Savings

Automation is one of the most significant tools for managing your finances. While you are going on vacation or trying to recover after a hurricane, automation makes sure all your bills and debt get paid and your savings and investments grow on autopilot. Automating your money has your money working for you while you sleep and simplifies your money system. There is even a book about how automation can make you a millionaire! Check out this blog post for more on automation and how it can improve your finances.

Calculate Your Net Worth

Subtracting liabilities from assets calculates your net worth, giving you a clear snapshot of your financial health. It shows how much wealth you've built and where you stand toward your financial goals. Your net worth is a powerful metric for tracking your financial progress with your budget and identifying areas for improvement, like paying down debt or increasing savings.

Invest for Retirement and Wealth

Even small contributions to retirement funds or investment accounts build wealth over time. Aim to contribute at least 1% of your income, increasing as you go. For more information on how to start investing, see the curated list of resources on the Suggested Reading Page.

Reassess Your Budget Regularly

Financial needs and goals change. Reviewing and adjusting your budget ensures you stay on track for your goals. Focus on these areas to improve your finances and make your money work for you. Some areas to focus on are the following:

- Pay off debt.

- Cut expenses.

- Save more money.

- Earn more money.

- Invest.

- Spend money intentionally.

TIPS FOR MAKING A BUDGET THAT WORKS FOR YOU

Creating a budget that aligns with your lifestyle and goals is critical to financial success. Here are some essential tips to help you build a budget that truly works:

Start Tracking Your Spending Before You Budget

If you’re new to budgeting, record your expenses. Tracking your spending will give you a clear picture of where your money goes, making it easier to start budgeting, identify areas for adjustment, and set realistic spending limits.

Automate Your Finances

Setting up automatic transfers for bills, savings, and debt payments removes the guesswork and lets your money grow on autopilot while you work, sleep, or enjoy life. It's like having a personal assistant who moves your money to help you accomplish your goals and earn millions over time.

Set Your Budget on Autopilot

The best budget runs itself! Once you automate your finances, your budget works quietly in the background, freeing up time for your other goals. Budget apps are great for putting your budget on autopilot. In addition to my Excel spreadsheet, I use Simplifi because I like the interface and net worth tracking feature. Simplifi is also adaptable to any budgeting style. However, there are several great budgeting apps to choose from. Find one that you like and helps you accomplish your financial goals with your budget.

Use Accounts That Help You Make Money

Choosing the proper accounts can boost your savings while keeping your money safe. Consider high-yield savings accounts (HYSAs) or money market accounts for emergency and sinking funds. These offer higher interest rates than traditional savings accounts and are FDIC-insured. My husband and I used a high-yield savings account at Wealthfront to help grow a “Family Emergency Fund” while planning our wedding.

You Can Still Budget If You Have Irregular Income

If you own a business or work for tips, budgeting can be tricky initially because you don’t have regular income every month. However, there is a way to budget for irregular income effectively. Create a primary account for all your income. From there, you can transfer a set amount to a separate personal spending account that covers fixed bills, day-to-day expenses, and savings goals. Keeping accounts separate creates financial discipline, making managing your regular and irregular income easier. I recommend automating your account structure to simplify your finances and budget.

Tiny Leaks Will Sink Your Budget

Tiny leaks in your budget, like unused subscriptions, overspending with impulse purchases, and unexpected fees, will sink your budget. Regularly reviewing your spending helps catch and eliminate these hidden costs. Tools like Rocket Money and Experian can help track down and cancel subscriptions you don't use. These small expenses can add up quickly, so monitoring spending is vital to avoid these money leaks regularly.

Get Rid Of And Avoid Debt To Free Up Your Budget

One of the most effective ways to create more room in your budget is to focus on paying off debt. Debt payments, especially high-interest ones like credit cards, can consume a significant portion of your monthly income. When I paid off my school loans, it felt like I got a huge pay raise in my budget that I could use for other goals like investing and a debt-free wedding.

Avoid accumulating more debt, or you’ll never break free of the debt cycle. Once the debt is gone, you redirect money into savings, investments, or other financial priorities, giving you more freedom to build wealth. For more on how to pay off debt in a way that works for you, check out this blog post.

Be Flexible

Budgeting guidelines like the 50/30/20 rule are helpful starting points, but adjusting them to fit your life is okay. For example, saving 10% of your income may not be possible during a significant life event, like replacing a car or having a baby. Adjust percentages as needed to stay aligned with your current circumstances.

If one budgeting style isn’t working for you and your goals, don’t hesitate to try another! For example, a zero-based budget can be helpful initially, but if it’s too restrictive, you may find a percentage-based or envelope method more comfortable. Finding a budget system that works for you within your life context is key.

Track Your Net Worth

Calculating your net worth measures financial progress. Tracking my net worth helped me realize that I was financially okay despite spending thousands on my wedding. As you budget effectively, reduce debt, and increase your savings, your net worth improves, which motivates you to stick with your budget.

Schedule Regular Money Dates To Review Your Budget

Set aside monthly time to review your budget and financial goals. These “money dates” will keep you engaged with your finances and allow you to make necessary adjustments as your life changes.

Progress Is More Important Than Perfection

Having a budget doesn't mean you manage money perfectly every month. Don't beat yourself up if you aren't perfect with your budget. Everyone has spending triggers that cause them to overspend. Each month differs from the next, so no budget will always be ideal. Focus on making progress with your finances. Grow your savings. Pay down and avoid credit card debt. Invest regularly. Grow your net worth. Spend within your means. Success with budgeting means your budget is helping you towards your financial goals, not that you are perfect with your budget style every month.

Mind Your Money Mindset

Your mindset around money significantly affects how well your budget works. Whether you make $10,000 or $10 million a year, if you consistently overspend or feel anxious about money, more money won’t make you feel better. Understanding the “why” behind your behaviors can create better money habits. Books like “The Psychology of Money” by Morgan Housel can offer valuable insights into how your mindset affects your money. You can also seek guidance from a financial coach, life coach, financial therapist, or certified financial planner who can help reframe your relationship with money.

CONCLUSION

Building a genuinely efficient budget requires understanding your unique needs and setting up a sustainable system to help you reach your lifelong financial goals. Try different budgeting styles and tools until you find a budget system that works for you. This approach will allow you to manage your finances confidently and build the future you’ve hoped for.

Are you ready to create a budget style that works for you?

Pin for later. Follow on Pinterest.