This post may contain affiliate links, which means I'll receive a commission if you purchase through my links at no extra cost. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure policy for more information.

Pin for later. Follow on Pinterest.

Pin for later. Follow on Pinterest.

INTRODUCTION

Debt can feel like a never-ending cycle, where you constantly use credit cards to cover expenses and then struggle to make payments. I paid off thousands of dollars in debt and learned several lessons along the way, but the most important thing to get out of the debt cycle is to know about it and take action to escape it. Understanding this cycle and learning to break free can help you repay debt for good. In this post, you will learn about the debt cycle and how to break free from debt with 15 key steps.

WHAT IS THE DEBT CYCLE?

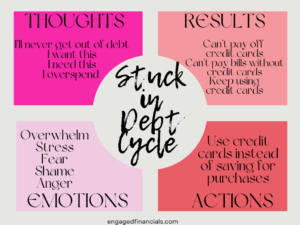

The debt cycle starts when you use credit to buy things you can’t afford. Whether it’s credit cards, loans, or financing offers, debt becomes a tool to make purchases when you don’t have the cash. This pattern often leads to a snowball effect, where the debt grows due to compounding interest, and you can't seem to pay it off in time. The balance keeps growing, and you must use more debt to afford your lifestyle. Even when you make the minimum payments, your debt keeps getting bigger because of compound interest, and you pay more than you originally borrowed. This happens over and over and over again until you become overwhelmed by debt.

HOW TO BREAK THE DEBT CYCLE AND PAY OFF DEBT

1. CHANGE YOUR ACTIONS TO CHANGE YOUR RESULTS

Commit to changing your financial habits and acting. Recognize that continuing to use debt will only worsen things and decide to make a change. Changing your life around debt is crucial to escaping the debt cycle. It’s easy to see credit cards as a safety net, but they can keep you stuck in a cycle of paying high interest rates and fees. Instead of using credit as a crutch, focus on budgeting, saving, and investing.

A vital component of the debt cycle is your thoughts and emotions, which drive your actions and results. Life coach Tonya Leigh discusses how your thoughts influence your money in her School of Self-Image program. Your thoughts make up your self-image, and if your thoughts keep you stuck in the debt cycle, then you will take action to reflect your thoughts of someone stuck in the debt cycle.

If you can change your thoughts about debt and take actions that support being debt-free, you can change your self-image into that of a woman who is becoming debt-free.

2. TRACK YOUR SPENDING

Tracking your spending is essential for breaking the debt cycle because it clarifies and controls your finances. By seeing exactly where your money goes each month, you can cut unnecessary expenses and redirect funds toward your debt. Budgeting apps like YNAB or Simplifi can help you track your spending, or you can check your bank statement every month. Knowing where your money is going helps you create a realistic budget that prioritizes debt payoff, making it easier to stay accountable and avoid falling back into debt.

3. CREATE A BUDGET

Once you know your spending habits, you can create a budget style that works for you. A budget can give you control over your finances by allocating your income toward essentials, savings, and debt repayment. Creating a budget is a powerful tool for crushing the debt cycle because it puts you in control of your money. By setting clear spending limits, you can avoid relying on credit cards or loans for purchases, preventing new debt from piling up. It also helps you track your progress, motivating you as your debt decreases each month. With a solid budget, you can prioritize paying off debt faster, build better financial habits, and ultimately break free from the cycle of debt.

I use a reverse budget, an Excel spreadsheet, and Simplifi to help manage my budget. However, there are several different budget styles and budgeting apps to choose from; find one that allows you to avoid debt and break free of the debt cycle. You can also use these principles to create a wedding budget and have a debt-free wedding.

4. AVOID CREDIT CARDS AND LOANS

When you rely on credit to cover everyday expenses or big purchases, it’s easy to fall into a pattern of spending money you don’t have, leading to high-interest charges and growing balances. Ultimately, avoiding new debt is crucial to achieving financial freedom and escaping the cycle for good. By cutting out credit cards and loans, you force yourself to live within your means, using only the available cash or savings to make purchases. Avoiding credit cards helps you develop healthier spending habits, prioritize essential expenses, and focus on paying down existing debt without adding more.

5. COMMIT TO A DEBT PAYOFF STRATEGY

Committing to a debt payoff strategy is essential for breaking the debt cycle because it gives you a clear, focused plan to eliminate debt. Whether you choose the debt snowball method (paying off smaller debts first) or the debt avalanche method (tackling high-interest debts first), having a strategy helps you stay organized and motivated. It ensures that you’re consistently making progress, no matter how small, and prevents you from feeling overwhelmed by your debt. Sticking to a structured plan builds momentum, reduces your debt faster, and avoids falling back into old habits of relying on credit.

Negotiating lower interest rates and consolidating debt are also options. By contacting your credit card companies and lenders to request lower rates, you can reduce the interest you pay overtime, significantly lowering your monthly payments. Additionally, consolidating multiple debts into a single loan with a lower interest rate simplifies your financial management and can make it easier to track expenses.

6. AUTOMATE PAYMENTS

Automating payments is a powerful way to break the debt cycle because it ensures you never miss a payment, helping you avoid late fees, penalties, and additional interest charges. When payments are automated, your bills and debt repayments are handled consistently, reducing the risk of falling behind or skipping payments due to forgetfulness or tight budgeting. This consistency helps lower your debt balance and boosts your credit score. Automating also simplifies your finances, giving you one less thing to worry about.

7. MANAGE SPENDING TRIGGERS

Managing spending triggers and avoiding overspending are crucial for breaking the debt cycle because they address the root cause of why debt often grows. Spending triggers—like stress, boredom, or people-pleasing—can lead to impulse purchases that add up quickly, pushing you to rely on credit to cover purchases. By recognizing and managing these triggers, you can make more intentional spending decisions, avoid unnecessary debt, and stick to your budget.

8. BUILD AN EMERGENCY FUND

An emergency fund is vital for breaking the debt cycle so you don't rely on credit cards for unexpected expenses. Using credit cards to cover emergencies like car repairs, medical bills, or home maintenance leads to new debt and high interest charges. Setting aside a small amount each month to build an emergency fund creates a buffer that helps you handle surprises. Even starting with a $1000 emergency fund can protect you from using credit cards when something unexpected happens. Saving helps reduce financial stress and lets you focus on paying down existing balances, making it easier to break free from the debt cycle.

9. USE SINKING FUNDS INSTEAD OF CREDIT CARDS

Sinking funds play a crucial role in breaking the debt cycle by allowing you to save in advance for planned expenses, which helps you avoid relying on credit when those costs arise. Setting aside a small amount each month for specific future expenses—such as savings for a wedding, holiday gifts, honeymoon, or car maintenance—creates a dedicated savings pool that prepares you for these financial needs. This proactive approach reduces the temptation to use credit cards or loans and promotes better budgeting and spending habits.

10. FIND WAYS TO SAVE MORE, EARN MORE, OR DO BOTH

Saving more money or earning additional income can help you break the debt cycle. Identifying areas in your budget where you can cut discretionary spending, such as dining out or subscription services, and redirect that money into a savings account.

Finding tools to help you save money can also help you crush your debt. Experian, a company that helps protect your credit by monitoring for suspicious activity, now offers tools to help you identify and cancel unused subscriptions. I love Rakuten and Capital One Shopping apps to help me save money while shopping online. Ibotta and $5 Meal Plan can help you save money on groceries with rebates and create affordable meal plans. Instacart also saves you time and money when grocery shopping by choosing what you want based on your meal plan.

Additionally, explore opportunities to earn extra income because there is no limit on how much you can earn. Getting a raise, answering surveys with Swagbucks, having a side gig, creating a blog, making a course with Teachable, or selling stuff on Shopify can significantly boost your income and help pay off debt.

11. TALK WITH YOUR PARTNER ABOUT YOUR DEBT

Talking about debt with your partner is the first step towards getting out of debt together. Scheduling regular “money dates” lets you discuss budgeting, spending habits, and debt repayment strategies. You can also have your money dates in a relaxed setting, making them less daunting and more enjoyable. Additionally, conducting a fall financial check-in provides an opportunity to assess progress, adjust your financial plan, and celebrate achievements together.

12. EDUCATE YOURSELF ABOUT PERSONAL FINANCE

Learning about personal finance equips you with the knowledge and skills to break free of the debt cycle. Understanding concepts such as budgeting, saving, investing, and the impact of interest rates can empower you to manage your money more effectively and avoid debt. Additionally, educating yourself about personal finance helps build confidence in your finances. Audiobooks and podcasts are a great way to learn about personal finance while living your life. Audible from Amazon is a great way to learn about money through audiobooks. Learning about money empowers you to break free from the cycle of debt and head towards financial freedom.

13. GET AN ACCOUNTABILITY PARTNER

An accountability partner is a powerful ally for staying motivated while paying off debt. When you share your debt repayment goals with someone you trust—a friend, family member, or financial coach—you create a support system to help you. Even just talking to your partner about debt can help keep you accountable. Regular check-ins can foster open discussions about budgeting, spending habits, and money-related emotional triggers. Your accountability partners will help you stay on track with your money goals.

14. REFINE YOUR MONEY SYSTEM

Refining your budget is essential for breaking the debt cycle to align with your goals and spending habits. By regularly reviewing money topics and adjusting your budget on your money date, you can identify areas where you may be overspending or where you can allocate more funds toward debt repayment. For example, using cash envelopes or digital budgeting tools like YNAB or Simplifi can make managing money easier. This refinement process allows you to create a system to prioritize paying off debt. As you refine your system, you build confidence in your financial decisions. Such confidence empowers you to break free from the debt cycle and achieve financial freedom.

15. CELEBRATE WINS

Celebrating wins is essential for crushing the debt cycle. Celebrations reinforce positive financial behaviors and keep you motivated along the journey. One effective way to track your progress is by watching your net worth improve as you pay down debt and increase your savings. As you see those numbers rise, it’s a tangible reminder of your hard work and commitment to becoming debt-free. Consider small rewards like having a nice meal, enjoying a day out, or indulging in a fun experience as a reward for each financial milestone you achieve.

CONCLUSION

Breaking free from the debt cycle isn’t easy, but it is possible. It starts with recognizing the cycle, shifting your mindset, and taking action to build new habits. These 15 key steps can help you break the debt cycle and finally pay off debt. You can become debt-free and escape the debt cycle for good!

IN SUMMARY

How To Break Free of the Debt Cycle and (Finally) Pay Off Debt

What is the debt cycle? The debt cycle is a pattern of overspending using credit cards or loans, which leads to debt accumulation and increased financial stress.

How to Break Free From the Debt Cycle

1. Change your actions to change your mindset.

2. Track your spending. Try budgeting apps like YNAB or Simplifi to help you.

3. Create a budget.

4. Avoid credit cards and loans.

5. Commit to a debt payoff strategy.

6. Automate payments.

7. Manage spending triggers to stop overspending.

8. Build an emergency fund.

9. Use sinking funds instead of credit cards.

10. Find ways to save more, earn more, or do both. Try Rakuten, Capital One, and Ibotta to save money. Earn money from Swagbucks, Teachable or Shopify.

11. Talk to your partner about your debt.

12. Educate yourself about personal finance. Use Audible to read books on the go.

13. Get an accountability partner.

14. Refine your money system.

15. Celebrate wins.

Are you ready to break free from the debt cycle?

Pin for later. Follow on Pinterest.